Empowering Black Voices in Finance: 6 Names You Should Know

- February 6, 2024

- Category: Blog, Budgeting, Debt, Financial Education

In honoring Black history throughout February and year-round, we’re spotlighting financial gamechangers whose voices are shaping the way we think and talk about money.

4 Steps to Take to Learn about Debt Settlement

Debt settlement is a process of negotiating with creditors to accept a percentage of the full amount on debt that is charged off or severely delinquent.

Alternatives to Bankruptcy

- September 12, 2023

- Category: Bankruptcy, Blog, Debt

There are bankruptcy alternatives that may make more sense for your situation. Learn about your options to avoid bankruptcy.

GreenPath’s Best Kept Secret – Recorded Webinar

- June 8, 2023

- Category: Blog, Credit, Debt, Financial Habits, Recorded Webinars

In the face of unexpected changes and inflation, many households have turned to credit cards to manage daily expenses and emergencies. See how a Debt Management Program can be a financial benefit.

Saldar sus Tarjetas de Crédito para Mejorar su Crédito y Alcanzar sus Sueños

Los precios siguen subiendo y con eso la presión en los presupuestos de las familias especialmente en la comida y la gasolina. Una encuesta reciente de NFCC y Wells Fargo demuestra que el 26% de los americanos están más preocupados con los gastos del hogar que hace 12 meses. Esto es debido a que los precios han subido...

Common Questions about Debt Management Plans

We receive a lot of questions when it comes to Debt Management Plans (DMPs). This article will answer all your common questions about what is a Debt Management Plan, its benefits and how it works.

Real Stories Ep 37: Finding Forgiveness: David Tackles Loans, Law School, and Supporting a Family

- March 15, 2023

- Category: Blog, College, Credit Card Debt, Debt, Financial Education, Loans, Podcasts, Real Stories

Podcast: Download (Duration: 54:45 — 43.9MB)

Subscribe: Spotify | Pandora | TuneIn | Deezer | RSS

David knows first-hand the importance of financial education and access to resources and opportunities. Listen to his story about tacking student loans, law school, and family.

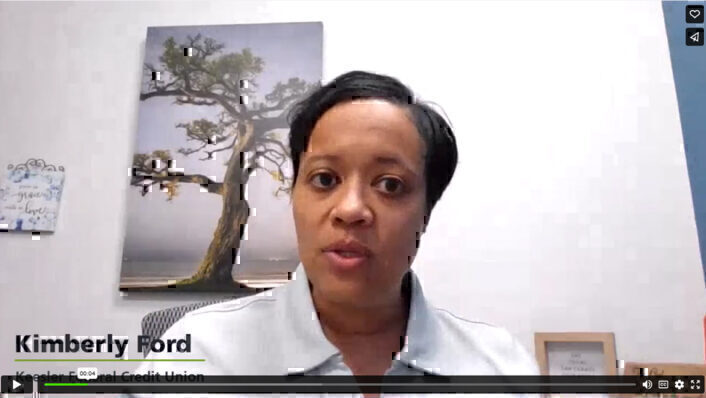

Follow The Green Brick Road: A Conversation with Kimberly Ford

- February 21, 2023

- Category: Blog, Debt, Financial Education, People Behind GreenPath

When it comes to money, the members of Keesler Federal Credit Union have a strong advocate in their corner: Kimberly Ford.

Advice for Couples with Different Money Personalities

While money talk may not be the most romantic thing you do in February, being on the same financial page with your partner is important. Learn how to match up your money personalities.

Showing results 1-9 out of 47