Debt consolidation loans and balance transfers are two effective strategies for managing and simplifying debt repayment.

Debt consolidation loans often offer lower interest rates and a fixed repayment schedule, while balance transfers provide temporary relief with low or 0% interest rates.

Both options have their own pros and cons, and the best choice depends on individual financial situations and goals.

The average American carries nearly $8,000 in credit card debt, according to data from The Federal Reserve and US Census Bureau. Dealing with debt can be overwhelming, but there are strategies to help you manage it more effectively. Two popular options are debt consolidation loans and balance transfers. Both can simplify your debt repayment process, but they work differently and have their own advantages and disadvantages.

What is a Debt Consolidation Loan?

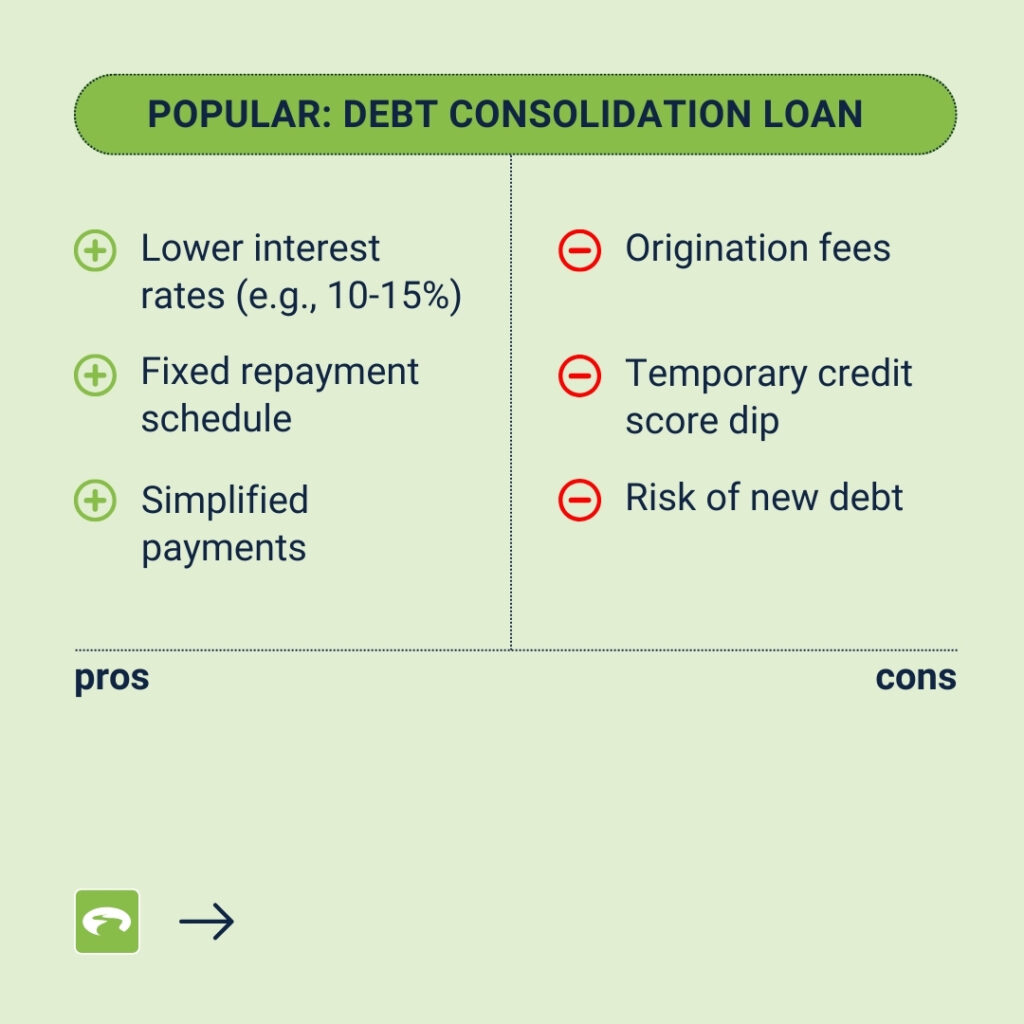

A debt consolidation loandebt consolidation loan involves taking out a new loan to consolidate debt and pay off multiple existing debts. This means you’ll have just one monthly payment to manage, often at a lower interest rate than your current debts. Personal loans for debt consolidation can be obtained from a credit union, which often offers lower interest rates compared to traditional banks. This can make it easier to keep track of your payments and potentially save you money on interest.

Debt consolidation loans can often offer lower interest rates compared to credit cards, which currently average above 20%. For example, a debt consolidation loan might offer an interest rate of around 10-15%, significantly reducing the amount of interest paid over time. Secured loans, such as home equity loans, can offer even lower interest rates due to the collateral.

However, it’s important to note that not all debt consolidation efforts are successful in the long term. A 2023 TransUnion survey found that consumers who opened a personal loan for debt consolidation often saw their credit card balances rebound to pre-consolidation levels within 18 months. This highlights the importance of disciplined financial habits post-consolidation. Debt consolidation can temporarily hurt your credit score due to credit inquiries, but proper management can lead to long-term improvements.

Pros:

- Simplified Payments: One monthly payment instead of multiple.

- Lower Interest Rates: Potentially lower interest rates compared to high interest debt like credit cards.

- Fixed Repayment Schedule: Clear timeline for paying off your debt.

Cons:

- Fees: Origination fees and other costs can add up.

- Credit Impact: Applying for a new loan can temporarily lower your credit score.

- Risk of More Debt: Without disciplined spending, you might accumulate new debt.

What is a Balance Transfer?

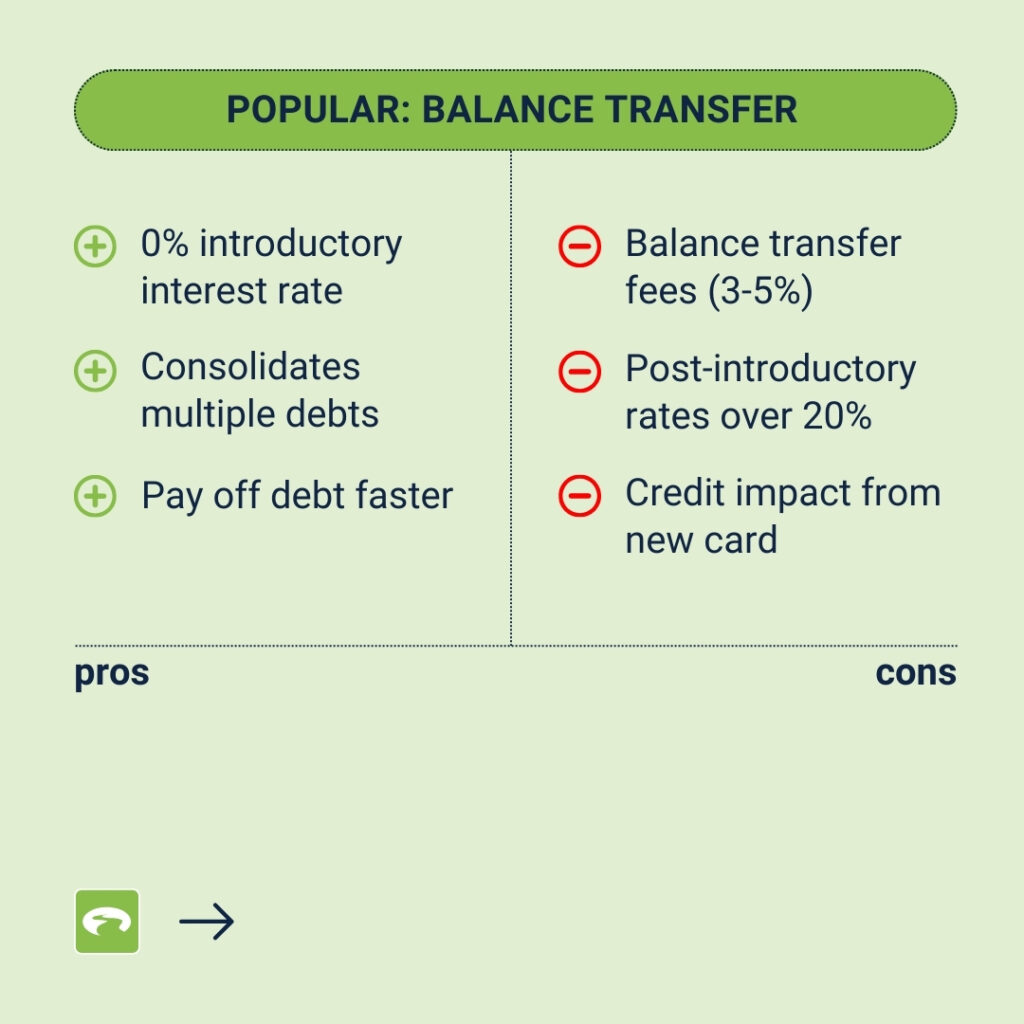

A balance transfer involves moving your existing credit card balances to a new credit card with a lower or 0% introductory interest rate. This can help you save on interest and pay off your debt faster, if you pay off the balance before the introductory period ends.

Balance transfers remain a popular option; however, these offers typically come with balance transfer fees ranging from 3-5% of the transferred amount. Additionally, after the introductory period, interest rates can jump significantly, sometimes exceeding 20%. Therefore, it’s crucial to have a repayment plan in place to avoid high-interest charges once the introductory period ends.

Pros:

- Low or 0% Interest: Save on interest during the introductory period.

- Simplified Payments: Consolidate multiple debts into one, making it easier to manage your finances.

- Potential Savings: Pay off debt faster with lower interest.

Cons:

- Balance Transfer Fees: Typically, 3-5% of the transferred amount.

- High Post-Introductory Rates: Interest rates can jump significantly after the introductory period.

- Credit Impact: Opening a new credit card can affect your credit scorecredit score.

Which Option is Right for You?

Choosing between a debt consolidation loan and a balance transfer depends on your financial situation and goals. Here are some factors to consider:

- Interest Rates: Compare the interest rates of both options. A debt consolidation loan might offer a lower fixed rate, while a balance transfer can provide temporary relief with 0% interest.

- Fees: Consider the fees associated with each option. Balance transfers often come with fees, while debt consolidation loans might have origination fees.

- Repayment Timeline: Think about how long it will take you to pay off your debt. A debt consolidation loan offers a fixed repayment schedule, which can help you become debt-free sooner, while a balance transfer requires paying off the balance before the introductory period ends.

- Credit Scores: Both options can impact your credit scores. A debt consolidation loan might cause a temporary dip, while a balance transfer can affect your score based on your credit utilization and new credit inquiries.

- Monthly Debt Payments: Combining multiple debts into a single loan can result in lower monthly debt payments due to reduced interest rates. This can provide financial relief and make it easier to manage.

GreenPath’s Debt Management Program for Consolidating Debt

GreenPath offers a Debt Management ProgramDebt Management Program which consolidates your debt into a single payment, often with lower interest rates and monthly payments. This program can help you pay off your debt faster and save money in the long run.

We work directly with your creditors and can often arrange lower interest rates and stop collection calls. By depositing money into your GreenPath account each payday, we manage your payments on your behalf, ensuring timely and consistent debt repayment. This structured approach not only helps reduce financial stress but also supports long-term financial stability.

The best choice depends on your specific financial situation, including your current debt levels, credit score, and ability to manage monthly payments. By carefully considering the pros and cons of each option and staying disciplined in your repayment efforts, you can take significant steps toward financial stability.

You Might Also Be Interested In…

Options for Dealing with DebtOptions for Dealing with Debt

What You Will Learn

- Different approaches to becoming debt free

- Preparation in tackling your debt

- How to achieve your debt payoff goals

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.