Credit counseling helps you manage debt and improve your financial health through personalized advice and support. When selecting the best credit counseling service, evaluate the range of services offered and the counselor’s qualifications to ensure effective assistance.

Working with a certified credit counselor can lower interest rates and reduce fees, making debt repayment more manageable.

GreenPath offers cost-free, judgment-free counselingcost-free, judgment-free counseling, helping you make informed decisions and achieve long-term stability.

Understanding Credit Counseling and Its Benefits

Feeling overwhelmed by debt? You’re not alone. With Americans collectively owing a record $1.17 trillion on their credit cards, many individuals are seeking ways to manage their financial burdens. The stress of mounting bills, high-interest rates, and the constant worry about making ends meet can take a significant toll on your mental and emotional well-being. It’s easy to feel trapped and unsure of where to turn for help.

Credit counseling offers a lifeline to financial stability and peace of mind. By working with a certified credit counselor, you can gain a clear understanding of your financial situation and develop a personalized plan to tackle your debt.

What is Credit Counseling?

Credit counseling is a service provided by certified professionals who help you manage your debt and improve your financial health. These certified credit counselors conduct comprehensive reviews of your financial situation to address both immediate debt challenges and the underlying causes of financial distress, ultimately offering tailored solutions such as Debt Management Programs, debt consolidation, or bankruptcy advice.

It is crucial to select the right credit counseling agencies by thoroughly researching their services and reputation to ensure they meet your specific needs. They work with you to create a tailored plan that addresses your unique financial situation.

Why is Credit Counseling Beneficial?

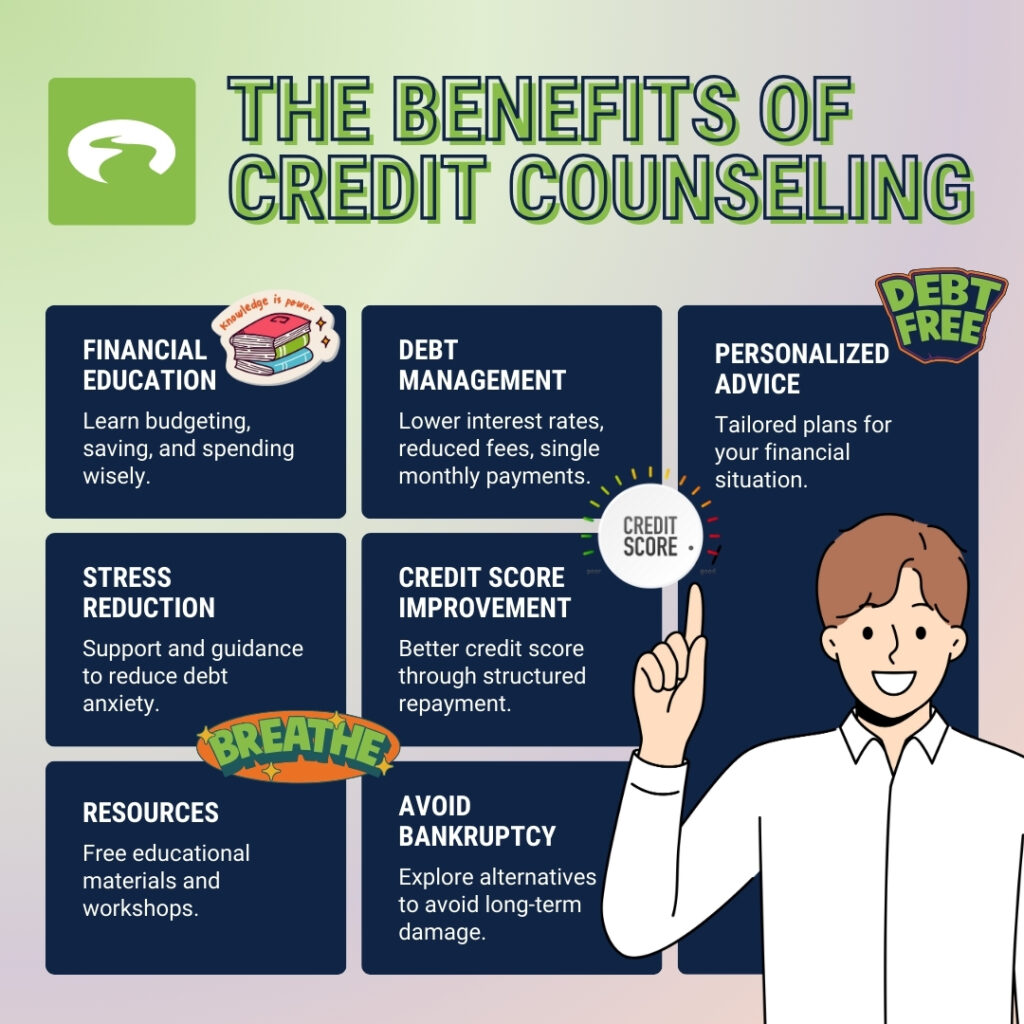

- Personalized Debt Management Programs: Credit counselors can work directly with your creditors to create a manageable repayment plan, known as a debt management programdebt management program. This often includes consolidating your debts into a single monthly payment, lowering interest rates, and reducing fees. The structured plan can help you avoid the pitfalls of missed payments and high-interest rates that can make debt seem insurmountable. By participating in a debt management program, you can also improve your credit history and achieve better debt management outcomes.

- Improved Financial Literacy: Credit counseling services provide valuable education on budgeting, saving, and spending wisely. This knowledge empowers you to make informed financial decisions and avoid future debt. Understanding how to manage your finances effectively is a crucial skill that can benefit you throughout your life.

- Stress Reduction: Dealing with debt can be stressful. Credit counselors offer support and guidance, helping you navigate your financial challenges with confidence and reducing the emotional burden of debt. Knowing that you have a plan and someone to turn to can significantly alleviate the anxiety associated with financial troubles.

- Positive Impact on Credit Score: By following a debt management program, you can improve your credit score over time. This makes it easier to qualify for loans and credit in the future. A better credit score can open doors to more favorable financial opportunities, such as lower interest rates on mortgages and car loans.

- Access to Resources and Workshops: Many credit counseling organizations offer free educational materials and workshops on money management, helping you build a solid foundation for financial success. These resources can provide ongoing support and education, ensuring that you continue to make wise financial decisions long after your initial counseling sessions.

- Avoiding Bankruptcy: For many, credit counseling can be a viable alternative to bankruptcy. By working with a counselor, you can explore options that may help you avoid the long-term consequences of declaring bankruptcy, such as damage to your credit score and the potential loss of assets.

- Tailored Financial Advice: Credit counselors take the time to understand your specific financial situation and goals. This personalized approach ensures that the advice and plans they provide are tailored to your needs, making it more likely that you will succeed in managing your debt and achieving financial stability.

How to Get Started with a Credit Counseling Agency

If you’re considering credit counseling, start by researching reputable organizations. Look for non-profit agencies with certified counselors, such as the National Foundation for Credit Counseling (NFCC). These organizations offer a range of services to help you regain control of your finances. The initial counseling session is a crucial first step, typically offered for free by nonprofit organizations, providing expert advice on your financial situation without any obligations.

GreenPath Financial WellnessGreenPath Financial Wellness is a trusted national nonprofit with over 60 years of experience and offers free financial counseling to help you manage your debt and improve your financial health. Our NFCC-certified counselors provide personalized advice and support, helping you understand your financial situation and develop a plan to achieve your goals. A free credit counseling session can be beneficial for individuals at any stage of their financial journey, offering valuable insights and assistance.

When choosing a credit counseling agency, it’s important to verify their credentials and ensure they are accredited by a recognized organization. You can also check for reviews and testimonials from past clients to gauge their effectiveness and reliability.

You Might Also Be Interested In…

Demystifying Financial CounselingDemystifying Financial Counseling

What You Will Learn

- How financial counseling works

- Who benefits from financial counseling

- What you can expect when speaking with a financial counselor

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.