Debt consolidation is a positive step, but it’s important to take additional actions to see improvements in your credit score.

Consistently paying bills on time, managing credit responsibly, and keeping balances low are a few strategies for rebuilding credit after consolidation.

If your credit score isn’t improving as expected, consider a Debt Management ProgramDebt Management Program for more structured support and personalized guidance.

So, you’ve taken the big step of consolidating your debt…kudos to you! But now what? Maybe you’re still waiting for that credit score boost you were hoping for. It’s completely normal to feel disappointed if your credit hasn’t improved as quickly as you’d like, but don’t lose hope. There are actionable steps you can take to set your credit on the right path.

Before we get into that, it’s important to understand how debt consolidationdebt consolidation affects your credit health. While consolidation can simplify your financial life by combining multiple debts into a single payment, its impact on your credit score isn’t always straightforward. Factors like hard credit checks, opening new accounts, and changes in your credit utilization can all play a role, making immediate improvements unlikely.

After consolidating your debt, it may take a few months of steady payments to start seeing changes in your credit score. The timeline varies depending on your credit history and the steps you take to rebuild. Remind yourself that consistent, positive actions can gradually turn things around—even if progress feels slow at first.

How Does Debt Consolidation Impact Your Credit Score?

Debt consolidation can simplify your finances by combining multiple debts into a single payment, but its effect on your credit score isn’t always immediate. Here’s why:

- Credit Checks: When you apply for a consolidation loan, lenders often perform a hard inquiry on your credit, which can temporarily dip your score by a few points.

- New Account: Opening a new loan or credit account adds to your credit mix, which can be beneficial in the long run, but initially, it can also lower your average account age, affecting your score.

- Credit Utilization: If your consolidation involves a credit card balance transfer, maxing out that new card could spike your credit utilization ratio. Ideally, you want to keep it below 30% of your total credit limit.

Remember, while debt consolidation is a step towards financial stability, it doesn’t erase the past. It’s crucial to focus on rebuilding credit to see long-term benefits.

How Quickly After Paying Debt Can You Expect Your Credit Score to Improve?

You’ve been diligently making payments on your consolidated debt…but how long before your credit score catches up?

- Immediate Effects: You might see small changes within a month or two as your payments are reported to the credit bureaus. However, the extent of improvement largely depends on your credit history and the amount of debt paid off.

- Short-Term Gains: Typically, within three to six months of consistent, on-time payments, you should start noticing a more significant uptick in your score. Keep in mind, negative items like missed payments or accounts in collections take time to fade in impact.

- Long-Term Recovery: If you’ve experienced severe credit issues like bankruptcy or foreclosure, recovery could take a bit longer—often 12-24 months. Persistence is key, and every positive action you take moves you closer to your goal.

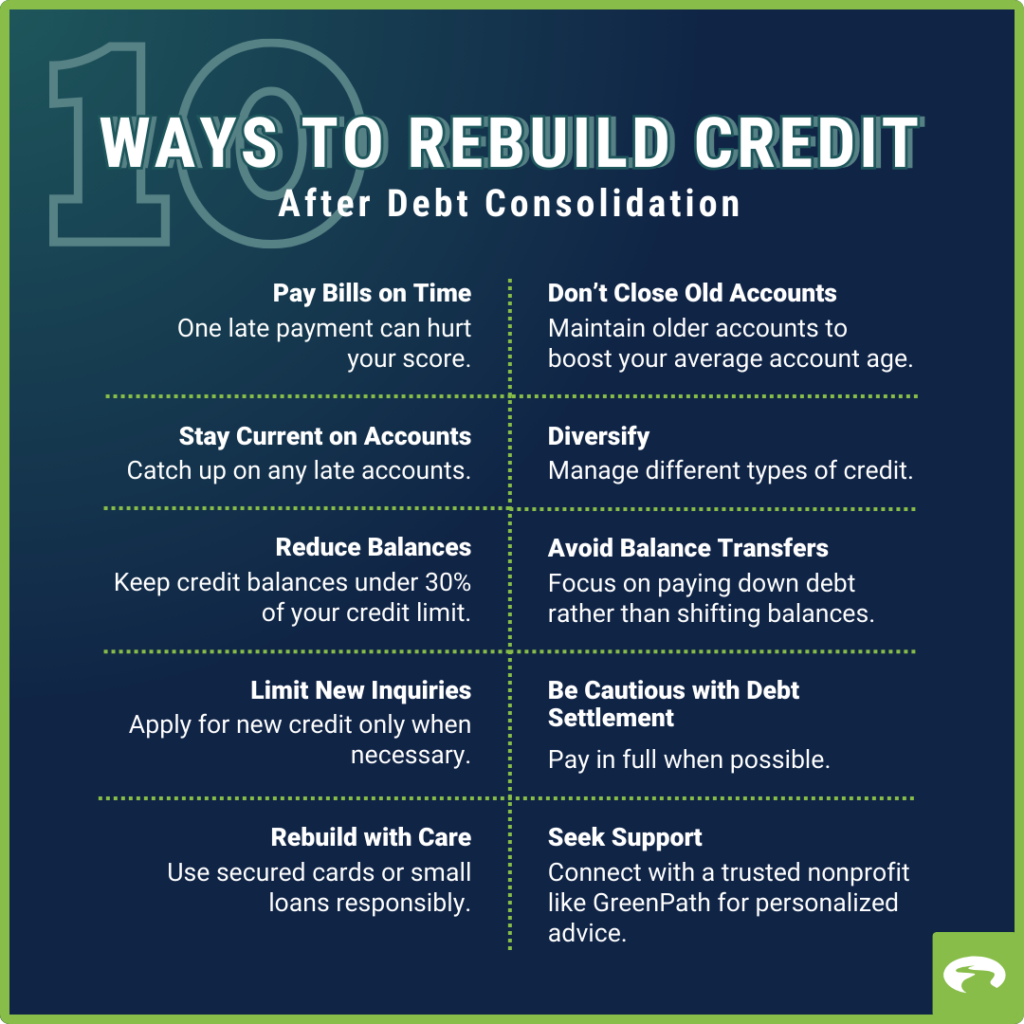

10 Ways to Rebuild Credit After Debt Consolidation

Now, let’s look at ways to rebuild your credit score after debt consolidation. These strategies will guide you in managing your accounts wisely and setting yourself up for a healthier credit future:

- Pay Bills on Time: Your payment history is the biggest factor in your credit score. Set up automatic payments or reminders to avoid missing due dates, even on utilities.

- Stay Current on Accounts: If you’ve fallen behind, get current and stay current. The longer you keep up with timely payments, the more your score will gradually improve.

- Lower Credit Card Balances: Aim to keep your balances below 30% of your credit limits. High balances can hurt your credit utilization ratio, so pay down those cards as quickly as possible.

- Avoid New Credit Inquiries: Each new credit inquiry can ding your score slightly. Only apply for credit when necessary and avoid tempting store card offers that promise quick discounts.

- Rebuild Credit Responsibly: Consider secured credit cards or small loans that report to all three credit bureaus. Use them wisely—make small purchases and pay them off each month to build a positive payment history.

- Don’t Close Old Accounts: Length of credit history matters. Keeping older accounts open (especially those with a good payment history) can help improve your score over time.

- Mix It Up: A healthy mix of credit types, like credit cards, auto loans, or mortgages, can positively influence your score. If you only have credit cards, consider a small personal loan, but keep those payments timely.

- Avoid Balance Transfers as a Crutch: Transferring balances from card to card doesn’t tackle the root problem and can lead to higher interest rates and fees. Focus on paying down your debts instead.

- Be Cautious with Debt Settlement: Settling a debt for less than what you owe might feel like a win, but it can stay on your credit report as “settled” instead of “paid in full,” which can hurt your score in the long run.

- Seek Professional Help: If you’re overwhelmed, don’t hesitate to reach out to GreenPath or a similar reputable non-profit credit counseling agency. They can offer personalized advice and might suggest a Debt Management Plan (DMP) that can help you manage payments effectively.

Transform your finances with GreenPath’s expert support. Take charge of your money starting now.

800-550-1961877-337-3399Debt Consolidation vs. Debt Management Program

While debt consolidation combines your debts into one, a Debt Management Program (DMP) through a non-profit organization like GreenPath offers more structured support. A DMP not only consolidates payments but also often lowers interest rates and provides personalized guidance on managing your finances. Improving your credit score isn’t an overnight fix, but with determination and the right guidance, you can make it happen.

GreenPath Financial Service

Free Debt Counseling

Take control of your finances, get tailored guidance and a hassle-free budgeting experience. GreenPath offers personalized advice on how to manage your money.